Profits earned from overseas forex trading are considered income in Japan, soonce you earn a certain amount of profit, you must file a tax return and pay taxes.

Tax returns are generally required to be filed between February 16th and March 15th of the following year, based on income earned from January 1st to December 31st of each year. It's a good idea to prepare in advance

Therefore, in this article, in addition to explaining how to file your tax return, we will also thoroughly explain various deductions and penalties to avoid losing money on taxes

Before we get to how to file your tax return for overseas forex trading, check this first!

Before looking at how to file your tax return for overseas forex trading, let's first understand what a tax return is

In essence, filing a tax return is "a procedure to report the amount of tax that should be paid to the government."

Tax filing is the process of calculating your income and tax liability for the period from January 1st to December 31st each year .

Since taxes are calculated based on income, if your taxable income for the year is negative, you do not need to file a tax return

However, if you have already withheld taxes or estimated tax payments, you will need to file a tax return so that any overpayment or underpayment can be settled

The tax filing period is generally set from February 16th to March 15th of the following year . It's a good idea to prepare in advance so you don't have to rush during the filing period

Failure to file a tax return will result in penalties

If you are required to file a tax return and fail to do so by the deadline, you will incur the following penalties and have to pay extra taxes

- Failure to declare taxable income will result

in a penalty tax of 15% to 20%. - If you file or pay taxes after the deadline,

a late payment penalty of 2.4% to 14.6% will - In cases of serious negligence such as concealing income, a heavy

penalty tax of 35% to 40% will be imposed. - If you file your return after the deadline, or if there are missing documents or concealment of information,

your blue return status may be revoked or your special deductions may be reduced.

Profits from overseas forex trading are also subject to Japanese income tax, so be sure to file your tax return correctly if you make a profit

You need to file a tax return if you are a salaried employee and your annual income exceeds approximately $1,250

If a salaried employee earns more than approximately $1,250 from overseas forex trading, they are required to file a tax return

Salaried employees

| Target audience | - Individuals who receive a salary from their employer, such as company employees or part-time workers.- Individuals who have income from public pensions, etc. |

|---|

Generally, if your only income is your company salary, you do not need to file a tax return because your company handles the calculation and payment of your taxes

However,if a company employee earns more than approximately $1,250 from overseas forex trading, or if a housewife or student earns more than a certain amount, they are required to file a tax return.

Please note that the conditions for filing a tax return include miscellaneous income other than that from overseas forex trading. If you have miscellaneous income other than from overseas forex trading, be sure to include it in the total

For business owners, etc., when the amount exceeds approximately $3,000

If you are self-employed or do not receive a salary, youare required to file a tax return if you earn more than approximately $3,000 from overseas forex trading.

Non-salaried workers

| Target audience | Unemployed individuals, self-employed individuals, housewives, students, and others who do not receive a salary |

|---|

Unlike salaried employees,non-salaried individuals are required to file a tax return if their miscellaneous income (profit minus expenses) exceeds approximately $3,000.

Unrealized gains and losses are not subject to taxation

Since only actual realized profits and losses are subject to taxation,unrealized gains and losses on positions that have not yet been closed are not subject to taxation.

Please note that swap points, which are received to hedge against interest rate and exchange rate fluctuations, will be subject to taxation once they are received and credited to your account

However, cashback is subject to taxation

Cashback received from FX brokers through account opening or deposit campaigns is subject to taxation

Generally,cashback is considered temporary income.

The taxable amount is calculated by subtracting the special deduction of approximately $3,125 from the temporary income and multiplying the result by half. If you have other temporary income, you need to file a tax return if the total taxable amount exceeds approximately $1,250

| Formula for calculating temporary income: Total temporary income - Totalexpenses - Special deduction (approx. $3,125) = Temporary income |

| Formula for calculating the taxable amount of temporary income: Temporary income × 1/2 = Taxable amount of temporary income |

Furthermore, since temporary income is subject to comprehensive taxation, thetaxable amount of temporary income is added to other income such as salary income when calculating taxes.

your taxable income from temporaryearnings exceeds approximately $1,250 for salaried employees, or approximately $3,000 for non-salaried employees, you are required to file a tax return.

Losses cannot be carried forward

Losses incurred from overseas forex trading cannot be carried forward to the following year and therefore cannot be offset against income in subsequent years

However, if you use multiple overseas forex brokers, you are allowed to offset income from other overseas forex brokers in the same year and calculate your taxable income accordingly

Furthermore, losses incurred in domestic FX trading can be carried forward for up to three years

| If you use three overseas forex brokers in the same yearBroker A: Loss of approximately $3,125 Broker B: Profit of $1,000,000 Broker C: Profit of $300,000

After offsetting the losses of company A (approx. $3,125), the profits of company B (approx. $6,250), and company C (approx. $1,875), taxes will be calculated on approximately $5,000 for that year |

| If you incur losses in overseas forex tradingYear 1: Loss of approximately $3,125 Year 2: Profit of approximately $6,250

Since losses from overseas forex trading cannot be carried forward, taxes will be calculated on approximately $6,250 in the second year |

| If you incur losses in domestic FX tradingYear 1: Loss of approximately $3,125 Year 2: Profit of approximately $6,250

Since losses from domestic FX trading can be carried forward, we deduct approximately $3,125 from the second year's profit of approximately $6,250, and then calculate the tax on the remaining approximately $3,125 |

Please note that overseas and domestic forex trading have different tax systems, so profits and losses from each cannot be offset against each other

If you want to keep your taxes down, declare your expenses

To minimize taxes on overseas forex trading, make effective use of your expenses

Taxes are calculated by multiplying the tax rate by the income amount, which is the profit from overseas forex trading minus expenses and income deductions

Therefore, if you incur expenses related to overseas forex trading,you can reduce your taxable income by deducting those expenses from your profits, resultingin lower taxes.

The more deductions you can subtract from your income, the greater the tax-saving effect and the lower your taxes will be. Therefore, when filing your tax return, be sure to include income deductions other than business expenses

Expenses are based on those "linked to sales."

When accounting for expenses related to overseas forex trading,you should base your calculations on expenses that are used specifically for overseas forex trading and are linked to sales.

Therefore, personal consumables used in daily life and private meal expenses are not recognized as business expenses

Furthermore, while the full cost of a computer and internet access dedicated to overseas forex trading can be claimed as a business expense, if you use it for both personal and business purposes, you must calculate the usage ratio andonly include the amount used for overseas forex trading as an expense.

If you are unsure whether an item qualifies as a deductible expense, contact your nearest tax office to confirm

How to file your tax return for overseas forex trading! A detailed explanation of the process

This guide provides a clear explanation, using images, of how to file your tax return for overseas forex trading

① Before filing your tax return, prepare your "My Number" and "Annual Profit and Loss Statement," etc

When filing your tax return, prepare the following four items

- Documents that show your My Number

- Annual trading report for overseas forex trading

- Receipts for necessary expenses

- Various deduction certificates

Those who have had their year-end tax adjustments done by their employer and have submitted the necessary deduction certificates do not need to submit them

<How to generate an annual profit and loss statement >

An annual profit and loss statement is a document that summarizes your trading history for a year, showing your profits and losses for that year

When filing your tax return, you'll need to have a grasp of your annual profit and loss, so be sure to prepare that beforehand

Here, we'll explain how to output data when trading using MT4 or MT5

- Open MT4/MT5 from your overseas forex account

- Open the "Account History" tab, right-click, and select "Specify Period"

- Specify the period for filing your tax return (for example, if you are filing your tax return in 2023, the period is from January 1st to December 31st, 2022).

- Right-click and select "Save Report" to save the data

This completes the output of the annual profit and loss statement

If you are a company employee, you will need your withholding tax statement

If you are a company employee or have other salary income, you will need your withholding tax statement

A withholding tax statement is a document issued by your employer that details your annual salary and other income

When filing your tax return for overseas forex trading, you will need to include your salary income in the calculation of your income tax, so be sure to prepare in advance

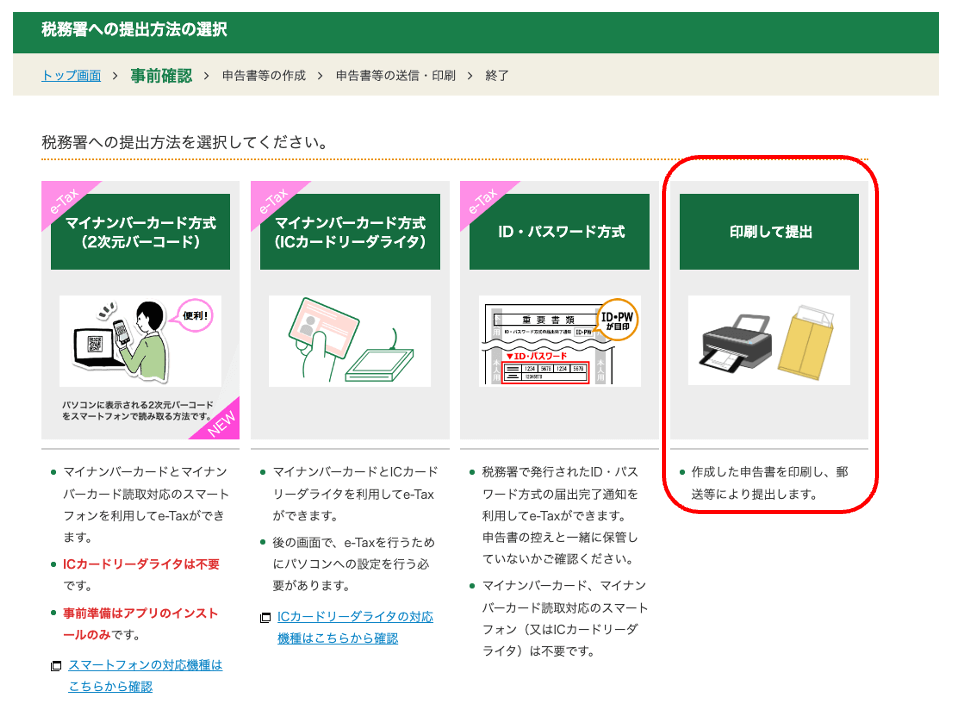

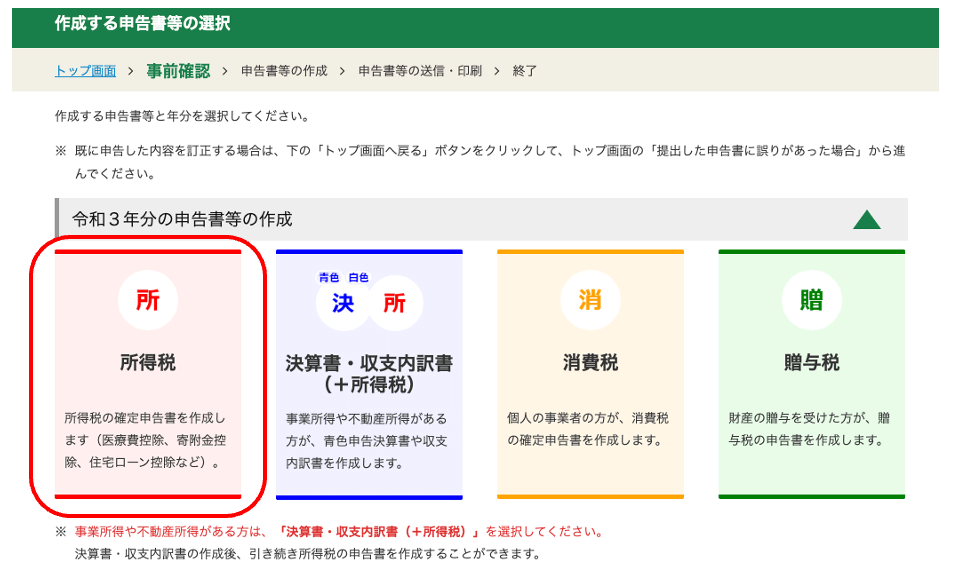

② Access the National Tax Agency's tax return preparation page

Next, we will prepare the necessary documents for filing your tax return

Access"Start Preparation"click the tax return preparation section and

This section explains how to print and submit your tax return. Click "Print and Submit"

③ Select "Income Tax" and start creating

Select the tax return form you wish to prepare

Select the year for which you will be filing your tax return, and then click "Income Tax"

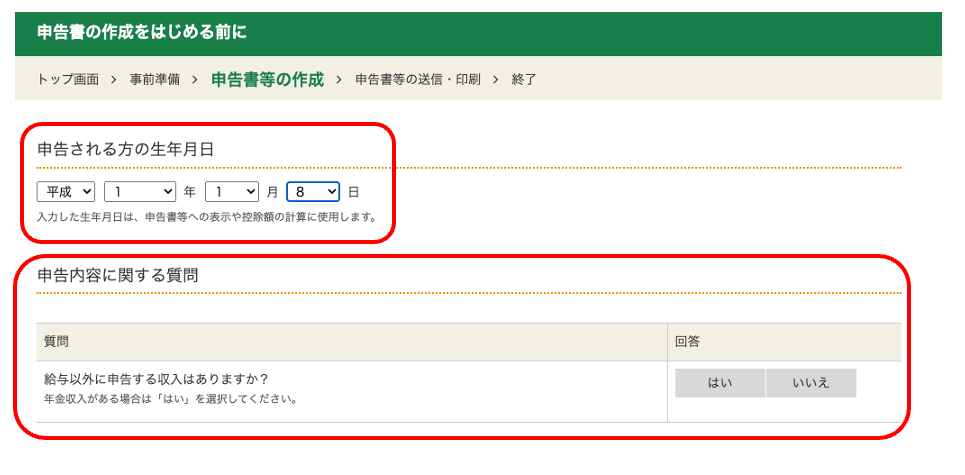

Before you begin preparing your tax return, you will need to select the person filing the return's "date of birth" and whether or not they have "income other than salary."

Now we'll actually begin the tax return filing process

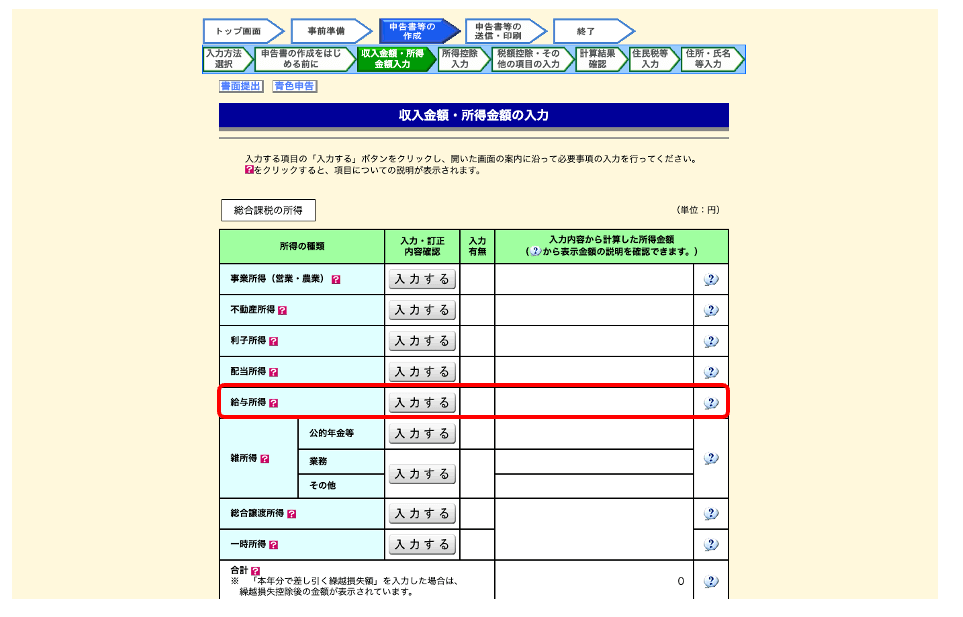

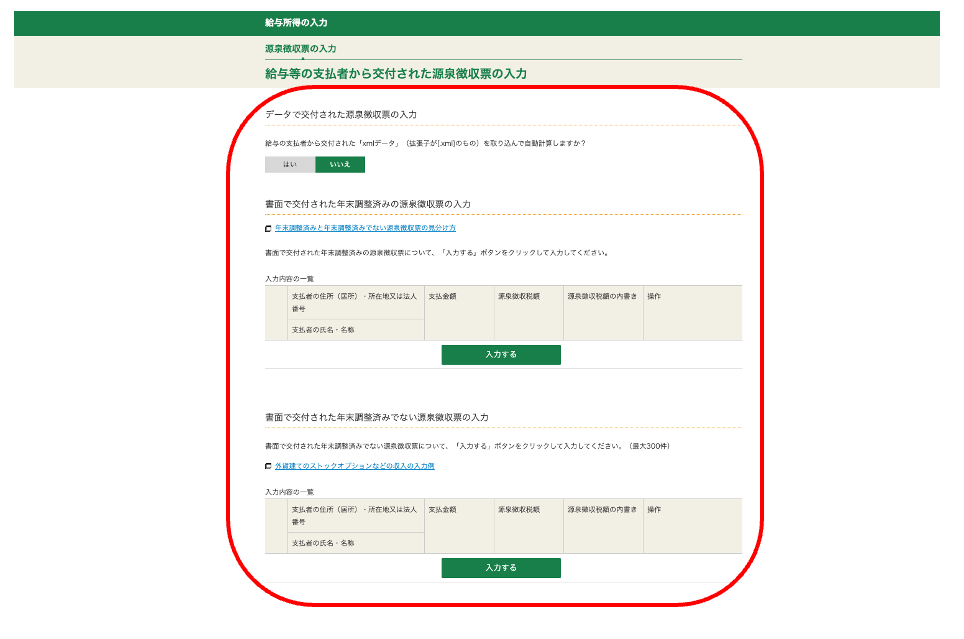

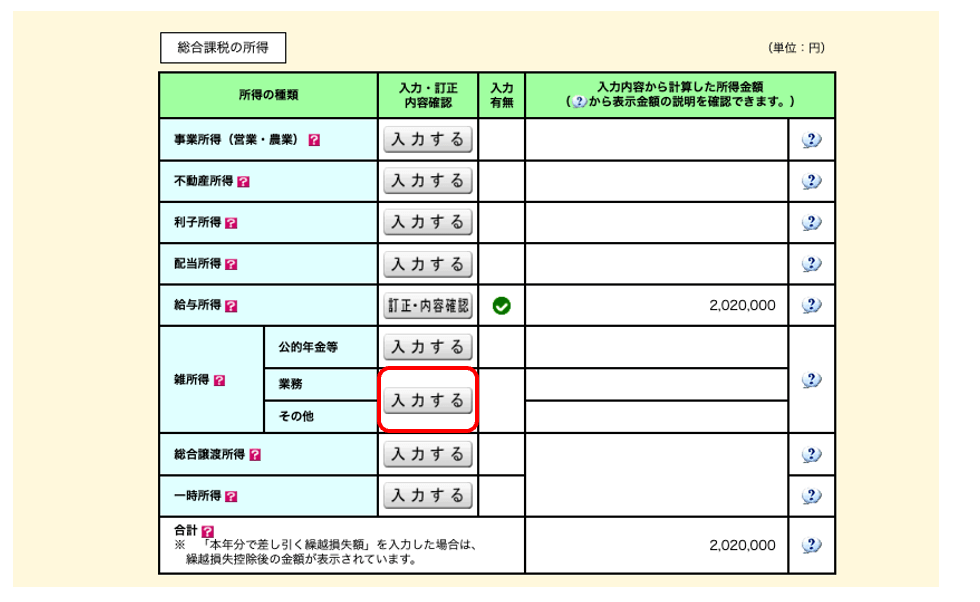

④ Enter your salary income and other details according to the instructions on the screen

Enter your income or earnings

Please enter your income if you have any income other than salary or overseas forex trading

Those with salary income should enter their information based on the withholding tax statement issued by their employer

This completes the input regarding salary income, etc

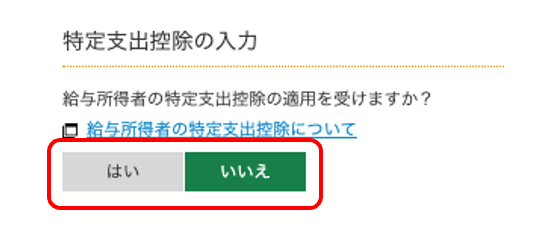

<What is a specific expense deduction?>

The specific expense deduction is a system that allows you to deduct business-related expenses from your income when you personally bear those expenses

If you personally bear the costs of the following seven items, you can claim a deduction as a specific expense

- Commuting expenses that are normally considered necessary

- Transportation expenses when working away from the usual workplace

- Relocation expenses due to job transfer

- Training fees for skills and knowledge necessary for the job

- Costs to obtain qualifications necessary for the job

- Transportation costs for employees working away from home to return home

- Books, clothing, and entertainment expenses necessary for work

However, proof from the employer is required to claim any of the specified expense deductions

If you are eligible for the specific expense deduction, select "Yes" for "Apply" and enter the information.

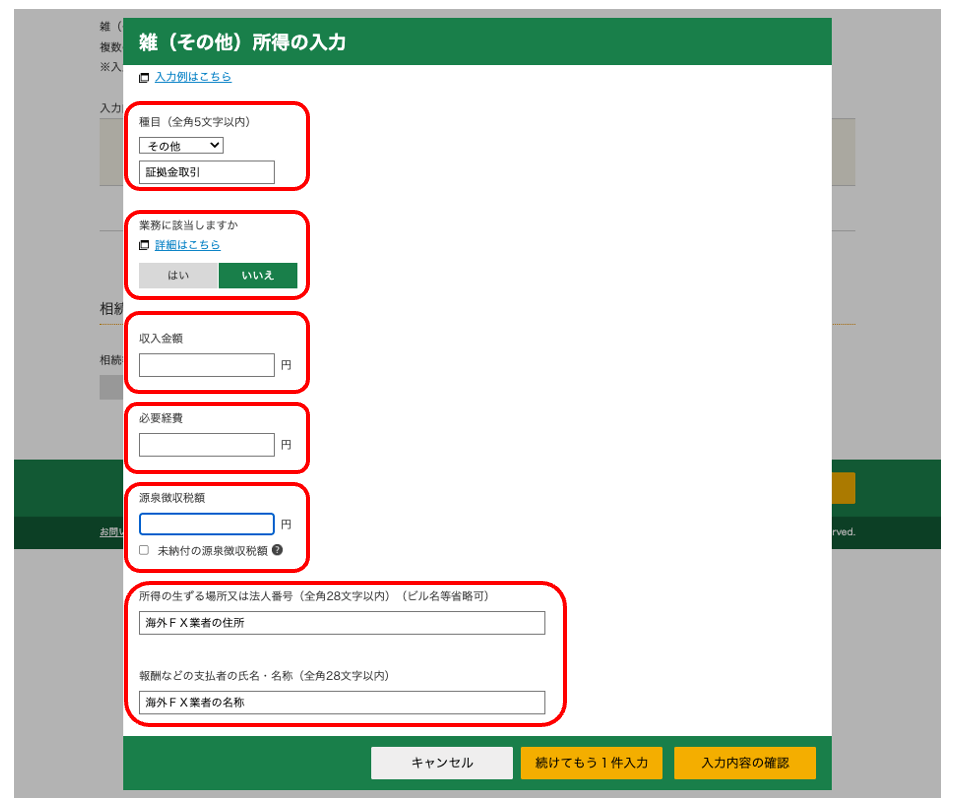

⑤ Enter the actual profits you earned from FX trading

When filing your tax return, enter any income earned from overseas forex trading, etc., in the "Miscellaneous Income" section

Enter your income from overseas forex trading, necessary expenses, and information about the overseas forex broker

This concludes the input regarding income from overseas forex trading

<Check the official website for the address of the overseas exchange

When registering your income from overseas forex trading, you will need to enter the address and name of the overseas forex broker. Please check the official website of the overseas forex broker and enter the information there

If you're unsure, please contact customer support

⑤ Enter any applicable deductions

If you are claiming various deductions such as medical expense deductions, life insurance premium deductions, or spousal deductions, please enter the applicable information

Since income deductions such as life insurance premium deductions and spousal deductions declared in your employer's year-end tax adjustment are already reflected in your withholding tax statement, you do not need to enter them here

⑥ Check the tax amount and proceed to the next step

Once you have finished entering your income deductions, the amount you need to pay will be displayed

Check the calculation results and proceed to the next step

⑦ Review the information regarding resident tax and business tax and proceed to the next step

After confirming the calculation result of the payment amount, please check the "Matters concerning resident tax and business tax."

After reviewing the content, we will proceed to the next step

<If you don't want your employer to find out about your side job, choose "pay it yourself">

In the resident tax input field, you can select the method for collecting resident tax on income other than salary and public pensions

If you choose special collection, the amount of resident tax incurred on your salary income and overseas forex trading will be notified to your employer, which could potentially reveal your side job

If you don't want your side job to be discovered, choose the "pay yourself" method for collecting your resident tax

⑧ Enter personal information such as address and name

You will need to enter personal information such as the address and name of the person filing the tax return

This completes the input of your personal information

⑨ Print your tax return

Finally, print out your tax return form and submit it to your nearest tax office either in person or by mail

This completes the tax return filing process

If you're unsure, it's a good idea to ask a tax accountant to handle it for you

If you are unsure about how to declare your income, expenses, and deductions, it is recommended to ask a tax accountant to handle your tax return for you

By hiring a tax accountant, you can not only file the correct tax return but also expect highly effective tax-saving strategies

Furthermore, you can consult with them about any concerns you may have, such as your business performance or tax reforms, and receive advice, which can help alleviate future anxieties

However, since this will incur fees for the tax accountant, you should consider whether the benefits outweigh the costs before hiring one

Q&A regarding how to file tax returns for overseas forex trading

Here are four frequently asked questions regarding how to file your tax return for overseas forex trading

- What is the tax rate on overseas forex trading?

- Do I need to file a tax return even if I haven't withdrawn any money from my overseas forex broker?

- Will I get away with not paying taxes?

- What is the going rate for completely outsourcing tax filing to a tax accountant?

Let's check the items that interest you

Q. What is the tax rate on overseas forex trading?

Profits earned from overseas forex trading are subject to comprehensive taxation, and therefore income tax is calculated using a progressive tax system.

Progressive taxation is a system where the higher your taxable income, the higher your income tax will be.5% to 45% depending on your taxable incomeTax ratesrange from

Income tax table

| Taxable income | tax rate | Deduction amount |

|---|---|---|

| From approximately $6.25 to approximately $12,181 | 5% | approx. $0.00 |

| From approximately $12,188 to approximately $20,619 | 10% | approx. $609.38 |

| From approximately $20,625 to approximately $43,431 | 20% | approx. $2,672 |

| From approximately $43,438 to approximately $56,244 | 23% | approx. $3,975 |

| From approximately $56,250 to approximately $112,494 | 33% | approx. $9,600 |

| From approximately $112,500 to approximately $249,994 | 40% | approx. $17,475 |

| Approximately $250,000 or more | 45% | approx. $29,975 |

Source: Income Tax Rates | National Tax Agency

Please note that the local tax on overseas forex trading is a flat rate of 10%

Q. Do I need to file a tax return even if I haven't withdrawn any money from my overseas forex broker?

Taxable income that requires filing a tax return is based on realized profits and losses. Therefore,even if you haven't withdrawn funds from your overseas forex broker, if your position has been closed and a profit has been generated, youare subject to filing a tax return.

Furthermore, if the total taxable amount of realized profits and losses exceeds approximately $1,250 for salaried employees, or approximately $3,000 for non-salaried employees, you must file a tax return

Q. Will I get away with not paying taxes?

Even if the income is taxable from overseas forex trading,if you don't file a tax return and pay taxes, the Japanese tax authorities will find out you've evaded taxes.

This is because Japanese tax authorities are supposed to be able to track income generated overseas through overseas remittance reports and the CRS (Common Reporting Standard)

A Report of Overseas Remittances is a notification form that you submit to the tax office when you deposit profits earned from overseas forex trading into a domestic account for use in Japan. The Critical Risk Management System (CRS) is a system designed to prevent tax evasion and avoidance using foreign financial institutions

If you fail to file a tax return, you will incur penalties such as a non-filing penalty tax, late payment penalty tax, and heavy penalty tax, and you will have to pay additional taxes

- Failure to declare taxable income will result

in a penalty tax of 15% to 20%. - If you file or pay taxes after the deadline,

a late payment penalty of 2.4% to 14.6% will - In cases of serious negligence such as concealing income, a heavy

penalty tax of 35% to 40% will be imposed. - If the filing deadline is missed, or if there are missing documents or concealment,

the approval for blue return filing may be revoked or special deductions may be reduced.

Profits earned from overseas forex trading must also be declared to the Japanese tax authorities, so if you have made a profit, be sure to file your tax return properly

Q. What is the going rate for completely outsourcing tax filing to a tax accountant?

The typical fee for hiring a tax accountant to file yourtax return is often determined based on your sales figures.

- Sales approx. less than $31,250; Commission approx. $625.00

- Sales: Approx. $31,250 or more, less than approx. $62,500. Commission: Approx. $937.50

- Sales: approx. $6.25 or more, less than approx. $93,750. Commission: approx. $1,250

By entrusting your tax filing to a tax accountant, you can reduce the amount of work involved in filing your tax return and ensure that you pay your taxes correctly

summary

This page explains how to file your tax return for overseas forex trading and how to avoid losing money on taxes

Finally, let's review the important points

- Tax returns are generally filed between February 16th and March 15th of the following year

- Failure to file a tax return will be considered tax evasion and will result in penalties

- If you are a salaried employee, you need to file a tax return if your income exceeds approximately $1,250. If you are not a salaried employee, you need to file a tax return if your income exceeds approximately $3,000

- Losses from overseas forex trading cannot be carried over to the following year

- When an employee files their tax return, they need the withholding tax statement issued by their company

It is also possible to ask a tax accountant to handle your tax return, so if you are unsure or don't want to spend time on it, using a tax return preparation service is recommended

Be aware that incorrect tax declarations or payments may result in penalties and additional tax bills